South Africa

South Africa Namibia

Namibia

David Knee

Co-Deputy Chief Investment Officer, Fixed Income (M&G UK)

A new financial equilibrium ahead?

This article was first published in the Quarter 3 2022 edition of Consider this. Click here to download the complete edition.

Key take-aways

- Developments such as the Covid-19 lockdowns, Russia-Ukraine war, Brexit and US-Chinese competition have all challenged the more open, globalised trends of the past four decades.

- Any reversal of these trends is likely to be an uneasy one for investors, with financial markets already reflecting sharp disruptions that have heightened risks and volatility.

- Although asset values are cheap across most areas, investors need to carefully assess the downside risks that have risen almost as quickly as inflation and interest rates. Extra caution is merited on all fronts.

- M&G has refrained from adding to our global and local equity positions, as we believe valuations need to cheapen further to compensate for the elevated risks.

In his book Homo Deus, A Brief History of Tomorrow, Professor Yuval Harari ponders a future for Humankind where knowledge is the new wealth and data the new religion. Computers, algorithms, and artificial intelligence create potential existential threats to life as we know it. Genetically and mechanically enhanced humans form a super race that would bode ill for those unable to afford an ‘upgrade’. You could at this point be forgiven for wondering if the author had abandoned his study of history for a career script-writing for the Terminator series, but this would be an error. Outlandish views of the future have a greater chance of being right than some notion of a tweaked version of today. Our human nature naturally inclines us to anchor to the recent past and extrapolate it far into the future. This tendency only serves to magnify the effects of the inevitable disturbances to the expected timeline.

Current global macroeconomic and political events have all the hallmarks of such a disturbance. I am reminded of when the Deathstar obliterated Alderaan in the first Star Wars movie and the perturbation in The Force was felt billions of light years away. The ‘balance’ was thrown out. Today our sense of financial balance has been built on 40 years of successful inflation fighting, falling real interest rates, rising globalisation, and increasing profit shares of GDP. In society, the corollaries have been massive reductions in global poverty, sharply rising real incomes but commensurate increases in global inequality. The net effect of all this is perhaps neatly summarised in one example: despite a five-fold improvement in living standards since 1950, people in Japan report being no happier now than then. Which raises the awkward question, how might we feel in a world of rising interest rates and rising inflation? And what might the path to this new equilibrium imply in terms of economic and market outcomes?

An uncertain path ahead

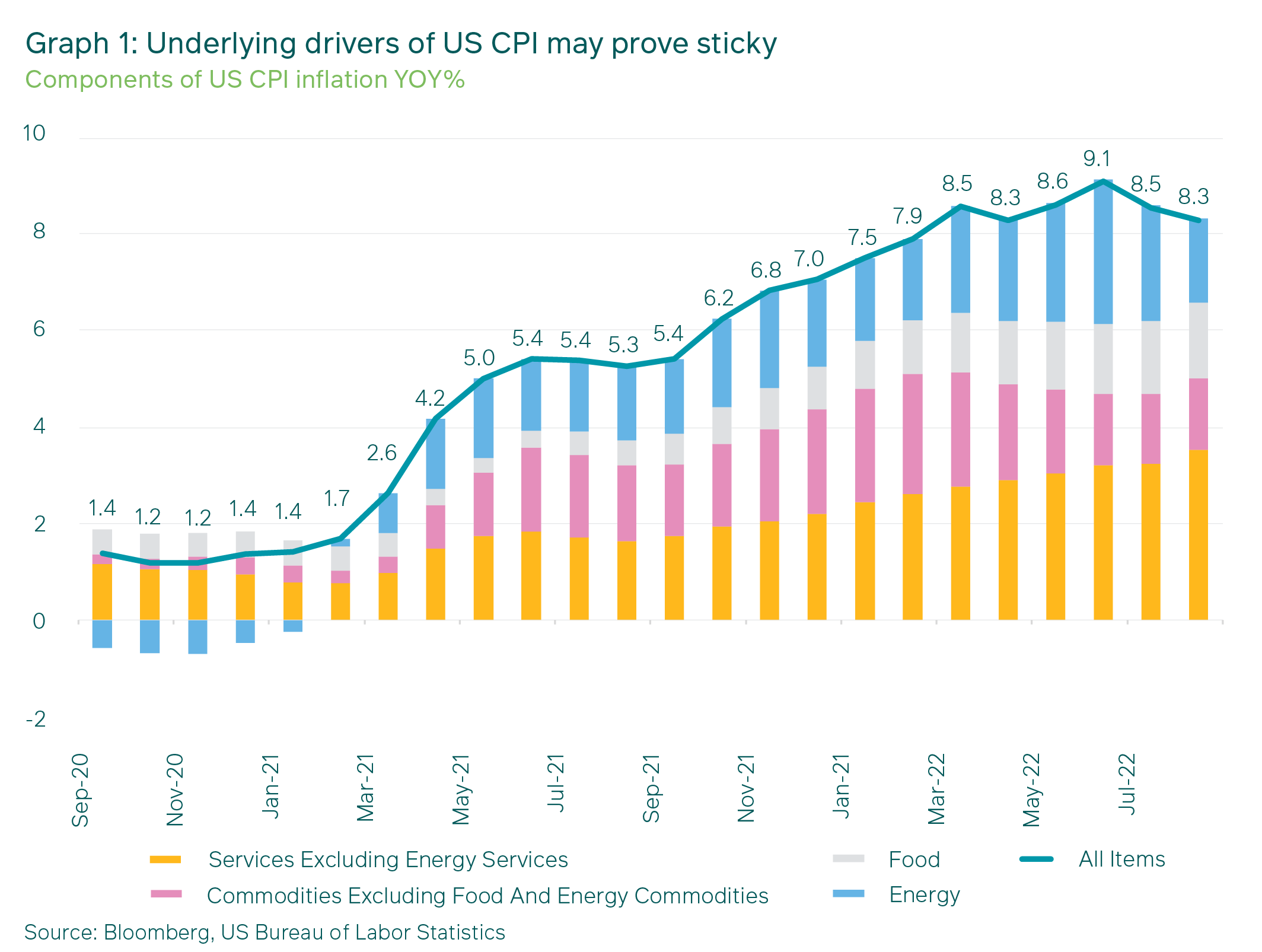

Of course, the answer is “we don’t know”. But I suspect at the very least, if that is where we are headed, the journey there isn’t going to feel good. In just a few months, economists have slashed their forecasts for 2023 European growth from +2.5% to +0.7%, with a clear bias to cut more. Equity and bond markets (and global central banks) have had to pivot from a view (which I shared, by the way) that inflation was a “transitory, supply bottleneck-driven phenomenon”, to a “don’t worry it’s just a temporary energy and food shock”, to an understanding that the primary engine at work here is now demand. Over 60% of the US inflation basket is rising at an annual rate of 4% or more. Excluding food and energy, US core inflation is zipping along at 6%, the highest since 1982.

Click chart to enlarge

Graph 1 illustrates how core goods and services, excluding the energy and food components, have still accounted for a substantial portion of the uplift in inflation; doubtless the US Federal Reserve is concerned that acceleration in these core components will unhinge long-term inflation expectations. Thoughts only a couple of months ago that we might see rate cuts before the end of 2023 have slipped from minds, leaving only a sense of unease that we don’t have a grip on what’s going on at all, and how could we have had such childish fantasies.

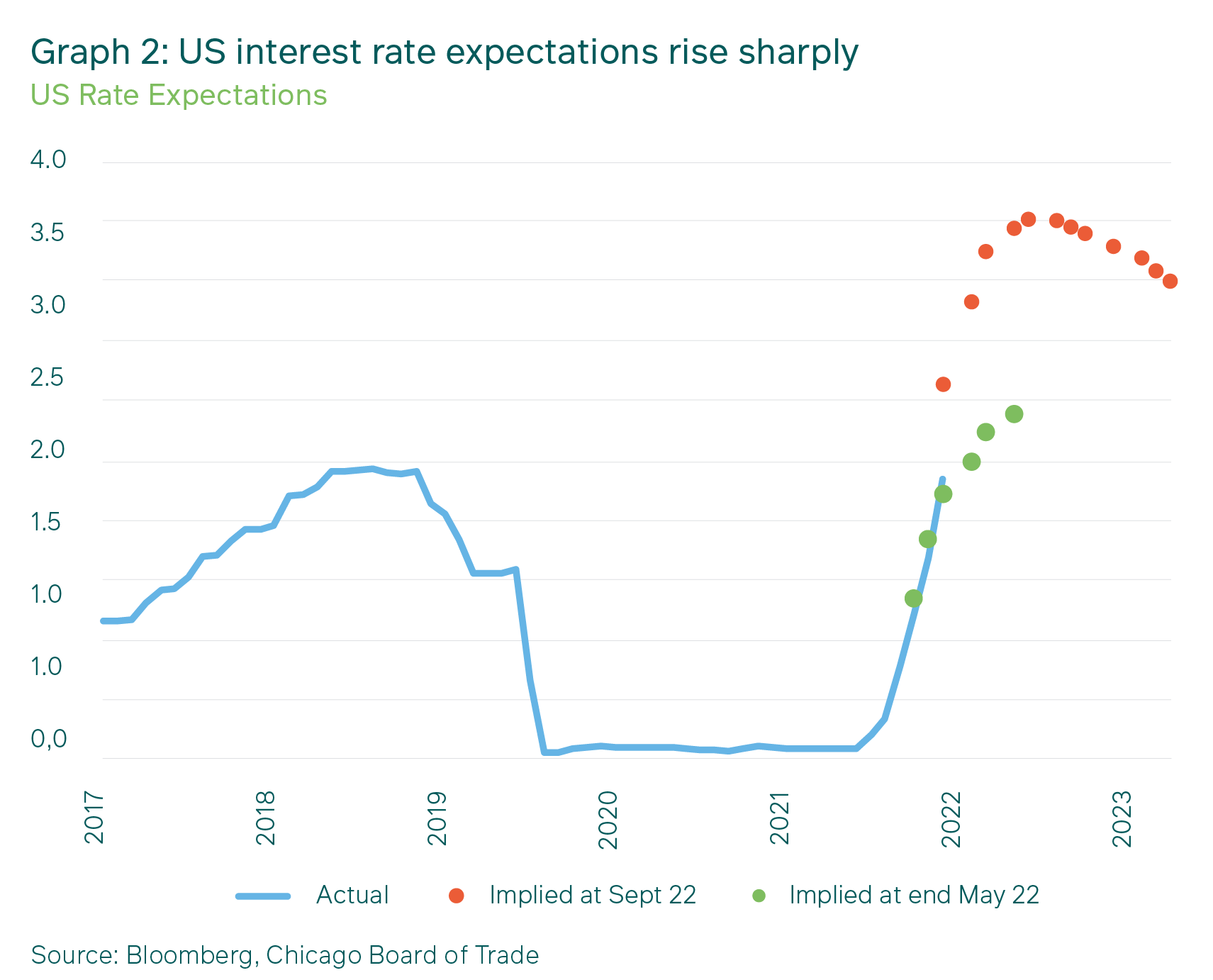

The result is intense market volatility, with sharp moves with each economic data release and with every speech by a Federal Reserve Governor. This is clear in the shift in Graph 2, which shows the move in short-term interest rate expectations in just the past three months. At the end of May, the forecast embedded in Fed Funds Futures contracts implied rates at 2.9% by mid-2023; that forecast is now for rates at 4.5%. The graph also highlights that investors expect rates will gently decline from there on. This may well happen, but equally, if inflation fails to fall back to more normal levels, further rate increases might still be needed, or at the very least, cuts are postponed.

Click chart to enlarge

Compounding our general unease, wasn’t it only the other day we thought that governments would be able to borrow at zero or negative nominal interest rates forever, and who cared two hoots about government debt when investors paid you to borrow? What happens if, in order to re-anchor inflation, cash rates need to return firmly into positive territory and debt is no longer “free”? Total indebtedness has not reduced at all since the Global Financial Crisis (GFC), so if rising rates enforce fiscal discipline and debt paydown in corporates and households, the result could be highly negative.

Keeping an eye on labour costs

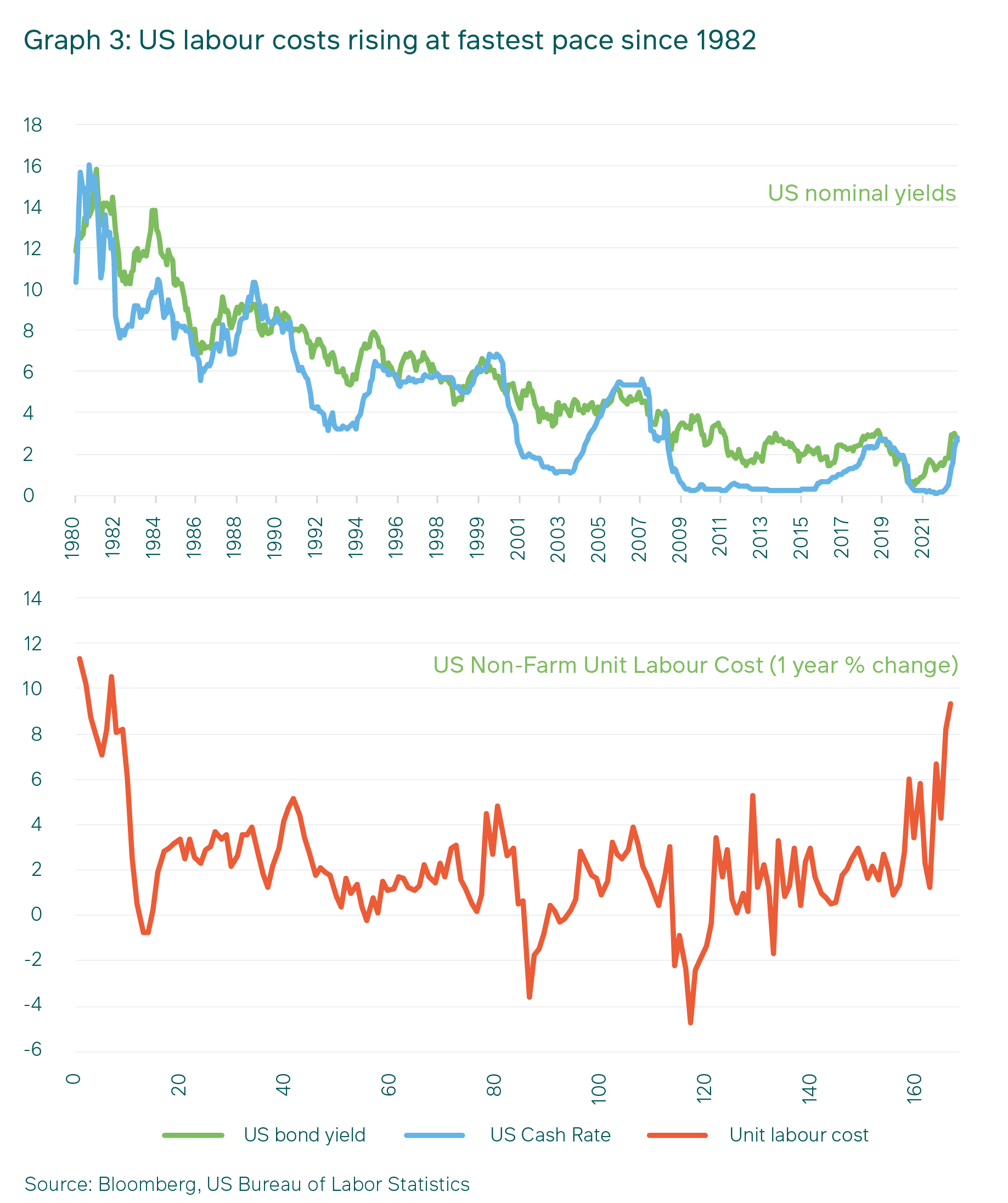

Key to the question of whether inflation is likely to become unanchored are near-term developments in unit labour costs, as shown in Graph 3. Wages per unit of productivity are a critical input cost for businesses, and therefore, when wages persistently rise faster than output, an underlying inflationary dynamic is likely to build that might prove painful to reverse. With the latest US Non-Farm Unit Labour Costs rising at 9.3% versus a year ago (also the highest rate since 1982), focus on this is understandable.

Click chart to enlarge

History may have something to tell us here, in that sticky wages were a key problem in the late ‘80s, the late 90s, and prior to the GFC, too. After a profoundly painful recession in the early ‘80s, Western labour markets were zinging along by 1988. On each of these occasions, the Federal Reserve had to raise interest rates until they were above (or very close to) the rate of growth in nominal GDP before an economic slowdown manifested and wages and inflation dropped. Needless to say, these episodes tended to go hand-in-hand with substantial rises in unemployment. The challenge right now is that nominal GDP is expanding at over 9% and interest rates are only at 2.5%. Nominal GDP will slow as inflation peaks and falls, but it still might leave a substantial gap that higher rates would need to fill if previous cycles repeat this time around.

We don’t know if this will happen. Inflation might instead fall sharply. In the past two decades, there was little obvious relationship between wages and unemployment, with a common explanation being that globalisation had broken local wage-setting frameworks and replaced it with a disinflationary impulse, courtesy of low wage rates in emerging markets. Factories and call centres were established in Asia and Eastern Europe, cementing a contract whereby advanced economies received cheap goods and services and in return, emerging economies generated jobs and rising living standards. This win-win relied on a stable geopolitical environment, in which in particular, peace prevailed.

Old global paradigms dented - or broken?

Russia’s invasion of Ukraine and China’s sabre-rattling and recent blockade of Taiwan have, at the very least, dented this contract. On-shoring and self-sufficiency in key goods like energy, food and defence are narratives that are building support, aided by the supply chain disruptions as countries emerged from pandemic lockdowns. Reducing Europe’s dependency on Russian energy is now a top political imperative and may well drive Europe into outright recession next year. In the US, Congress recently passed a bill providing US$50 billion of support for the US semi-conductor industry, recognising that the country doesn’t want to be held to ransom if Taiwan is prevented from supplying these vital inputs for the global economy. As a by-the-by, there are about 200 chips in one Javelin anti-tank missile.

Exercising caution in global equities

Against all of this uncertainty, how does one invest? If the advanced economies nudge into recession in 2023, equity earnings are at risk. The magnitude of any earnings downgrades would be amplified if interest rates are still rising due to sticky inflation. At M&G we absolutely consider this as a risk scenario and we examine the robustness of our portfolios should it prevail. But this is not our starting point. The outlook can be challenging, but valuations can compensate for the prevailing risks -- not all risks or scenarios of course, but if valuations offer decent levels of protection against adverse outcomes and compelling returns in muddle-through or favourable outcomes, then the right investment action, in our view, is to stay invested. This is our conclusion in terms of global equities. Valuations have become significantly more exciting given the market declines this year. Many markets are very cheap in all circumstances except a hard recession, and even then pricing suggests losses would be short term and not permanent. Hence we have been happy to keep a neutral weighting in this asset class, despite the risks.

SA equities: It’s about tomorrow, not yesterday

The narrative around South Africa equities is rather different. Since March 2013, just before the Taper Tantrum, the FTE/JSE Shareholder Weighted Index (SWIX) has delivered 8% per annum to investors, bonds 7% and cash 6%. Inflation over the near-decade-long period averaged 5%. Suffice to say, real returns have been disappointing and investors feel they haven’t been compensated for the volatility. Little wonder that it has been cash and near-cash funds that have taken R400 billion of inflows in the past four years or so, while General Equity funds have seen zero. Of course, you would have done blindingly well pivoting from cash to equities in April 2020, but no one was inclined to do so, according to the unit trust flow data. It’s a point that we make often at M&G: you are unlikely to be able to time the market successfully, and when it feels most difficult to pivot, the odds are that it will actually have been the best time to do so going forward.

Still, investing is all about tomorrow, despite the fact that how we feel about our portfolios and their positioning is all about yesterday. The fact that South African equities have disappointed hasn’t been because they have lacked earnings growth. Indeed, aggregate earnings have tripled since March 2013. So what happened? There are two key drivers in our view: First, the market was on an expensive multiple in early 2013. The world thought interest rates would be held at zero forever and then Ben Bernanke thrust his spanner into the wheel with his taper announcement. SA equities (and the rest of the world) needed to normalise valuations. But the second driver has been a shift in risk appetite, both as a global phenomenon and due to idiosyncratic SA factors.

Slowing SA growth, rising indebtedness, credit rating downgrades, corruption, load shedding, riots, water rationing, grey listing and many other issues have driven risk appetites down. While each of these factors is worthy of an article in its own right, in our view the net result is they have caused a disconnect to emerge between the earnings-producing ability of SA companies (with much of those earnings coming from outside SA, remember) and their valuations. The market is currently close to the cheap valuation levels it reached in the GFC. There are never any guarantees in markets, and a global recession next year could delay things somewhat, but from this starting point the odds are massively in favour of above-normal returns from our own equity market. With the growth and inflation risks around the world that were highlighted earlier, this isn’t the time to be maxing out risk positions, but valuations support an overweight stance in our view, with further capacity to add to this if growth does temporarily slow into next year.

Share

Did you enjoy this article?

Get the Newsletter

Get the Newsletter