South Africa

South Africa Namibia

Namibia

Pieter Hugo

Chief Client and Distribution Officer

Don't be tempted by cash returns

In recent times, South African investor confidence has been undermined by the news spotlight on the country’s higher political and economic uncertainty. This has been compounded by poor returns from local equities, which have underperformed money market returns over the past three years and not beaten inflation in the past two years (to 31 May 2017). These conditions, in turn, have pushed investors to sell their local equity holdings and other risk assets, and move more into cash. However, this is a serious mistake – cash is the more risky asset for long-term investors.

To 31 May 2017, the average SA General Equity fund returned only 0.4% p.a. over one year and 3.6% p.a. over three years (both after fees), underperforming the average Money Market fund return of 7.8% p.a. and 7.0% p.a. respectively (after fees). Yet this should be recognised for what it is: a short-term cycle. Over the past 40 years, South African equities have returned 8.2% p.a. on a real (after-inflation) basis, much higher than the 2.8% p.a. real return delivered by SA bonds and the 1.8% p.a. real return from cash. This makes them an invaluable part of an inflation-beating portfolio over time and gives investors a compelling reason to hold them through the downturns.

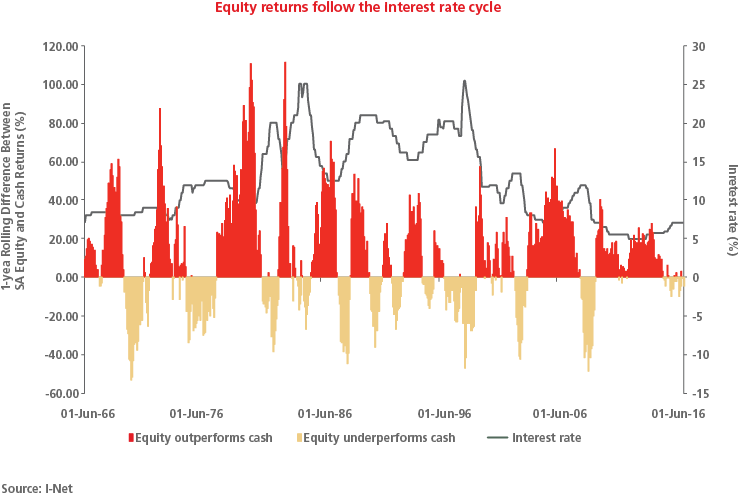

The graph, dating back to 1966, highlights how there have been many similar periods like the present during which equities have underperformed cash, with returns broadly following the interest rate cycle (the latter shown by the black line). (Red indicates periods where equities have outperformed cash over the preceding 12 months; gold depicts underperformance). It demonstrates how, although local equity returns do soundly beat cash over time, they underperform during relatively short periods, especially when interest rates rise, only to beat cash again as interest rates are falling. This underperformance is particularly evident when interest rates peak, as is the case currently. Based on this historic cyclical pattern, equity returns could begin to outperform cash again as our interest rates fall. And it’s worth noting that the Reserve Bank has indicated no further interest rate hikes are likely in the current cycle.

A closer examination of the asset return cycle in 2003-04 shows that the average SA General Equity fund, with a 12-month return to 30 April 2003 of -15.7%, badly underperformed the average Money Market fund’s 12.2% return (both after fees) over the same period. However, 12 months later this was reversed: the average SA General Equity fund returned 50.3% for the 12 months to 30 April 2004, while Money Market funds returned 10.5% on average. Had investors decided to switch their equity exposure to cash following the poor 2003 equity returns, they would have missed out on its exceptional returns the subsequent year. And there are many other examples of these short-term turnarounds in asset returns (1998-99, 2008-09, etc.), due partly to the quick impact of moves in short-term (three-month) interest rates. It is impossible for investors to be able to foresee such turns in the cycle with 100% accuracy and take full advantage of them. This means that they miss out on periods of improving equity market returns. Therefore investors’ best option for successfully building wealth is to hold their equity exposure through cycles, over the longer term.

For more information or if you have any questions, we recommend getting in touch with a good independent financial adviser. Alternatively, please feel free to contact our Client Services Team on 0860 105 775 or at query@prudential.co.za.

Share

Did you enjoy this article?

Get the Newsletter

Get the Newsletter