South Africa

South Africa Namibia

Namibia

Sandile Malinga

CIO Multi-Asset

Navigating regime shifts and market dynamics

As investors navigate an evolving global economic landscape, it's important to understand how recent perceived shifts in inflationary regimes, and the resultant monetary policy actions taken by central banks, may impact asset pricing and the resultant asset allocation decisions. The COVID-19 pandemic has catalysed a dramatic shift in inflation dynamics, moving from a period of relative price stability to one of heightened volatility. This regime shift has significant implications for sentiment, asset pricing and investment strategies.

The global inflation landscape

The post-GFC period before the pandemic, was characterised by inflation rates, especially in major economies like the US, were relatively stable, hovering around 2%. However, the pandemic disrupted global supply chains and caused significant supply and demand imbalances. Lockdowns initially reduced demand, but once economies reopened, there was a surge in demand for goods, which exacerbated the supply constraints. This imbalance drove up inflation across goods, wages and services, resulting in a broader increase in headline inflation.

In response, the Federal Reserve has tightened monetary policies to combat rising inflation. Despite relatively stable inflation expectations, central bankers are clearly concerned about inflation's persistence. This shift raises the question of whether a 3% inflation rate is the new 2%, to which the global economy had become accustomed. Although precise forecasts on where inflation may be settling are almost impossible, understanding how this regime shift impacts asset pricing is crucial.

Market sentiment has been characteristically volatile, with significant fluctuations in market pricing of future rate moves, following the US inflation report in July. Speculation about the size and timing of rate cuts has been a feature. At the start of the year, the market was fairly certain of a rate cut by March 2024, however, growth and inflation data emerging conspired to delay delivery of these rate cuts further and further into the year. Now the market is once again convinced that a rate cut will be delivered by September, with the size of the cut being the point of debate of late. This goes to highlight just how volatile shifts in market beliefs and expectations have been.

The long end of the term structure, where the effects of monetary policy should be less impactful compared to the front-end, has also had its fair share of volatility. Long-dated US Treasuries, say the 10-year and 30-year, have seen yields sell-off by 300 basis points from their post-COVID lows, signalling a dramatic shift in the global cost of capital. In previous episodes where the yield curve (say the yield of a 10-year bond minus the yield of the 2-year bond) inverts, the proverbial market wisdom starts expecting a profound slowdown in economic activity. This hasn’t been the case in the post-COVID world, further confusing the market and beliefs. In fact, what we’ve observed unfolding through 2023 and 2024 is an economy and labour market in good health.

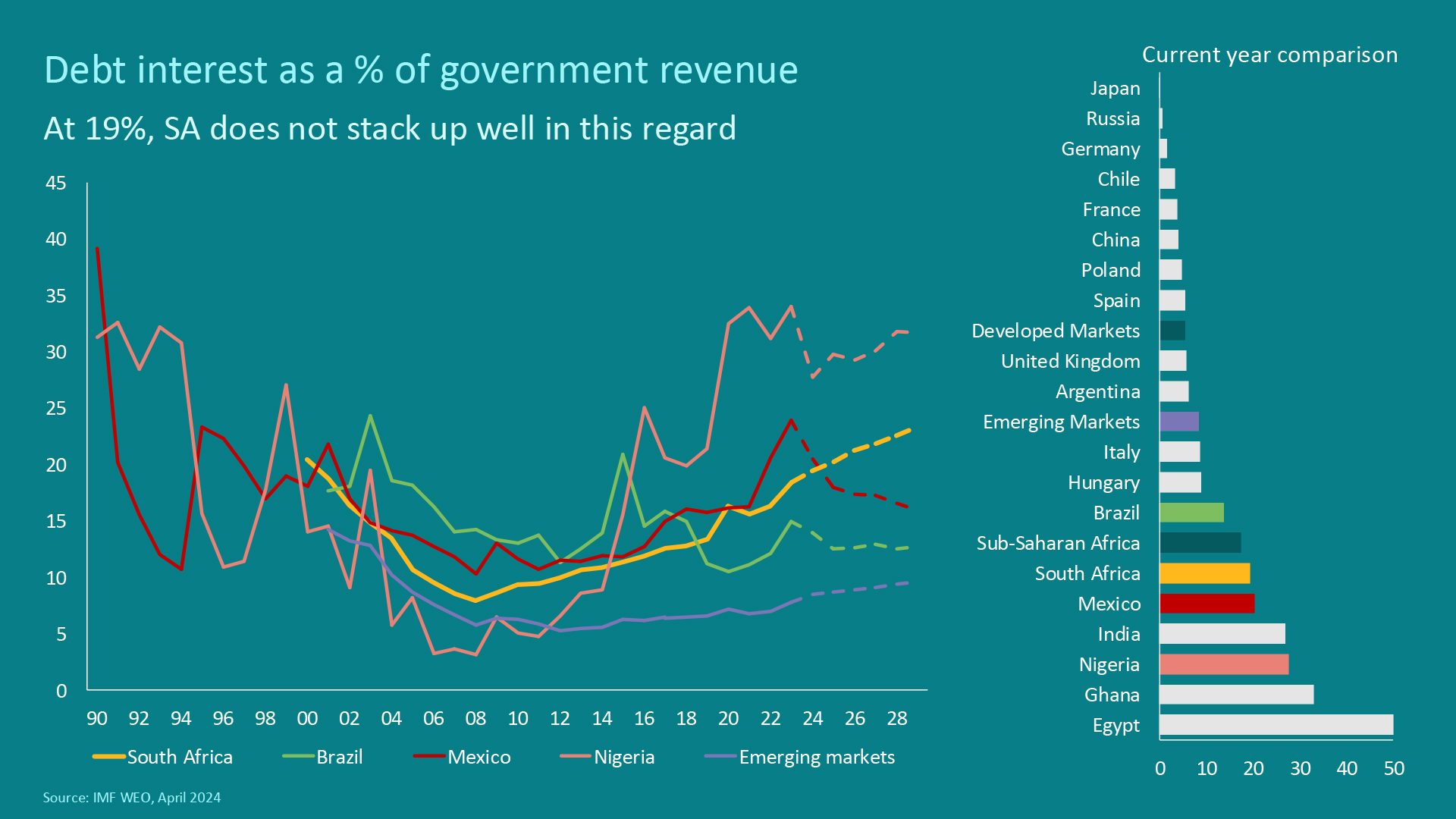

South Africa's debt and economic dynamics

Locally, South Africa faces its own unique economic challenges, particularly with high government debt levels and rising interest rates. The country currently uses 20c of every R1 collected in revenue to service its debt. This is unsustainable and crowds out necessary investment spending. Addressing this issue requires both lowering yields (via higher market and investor confidence driven by measurable gains in structural reform) and reducing the level of government debt as a percentage of GDP. The path to debt sustainability lies in achieving higher and more broad-based levels of economic growth.

The government’s structural reform initiatives, notably Operation Vulindlela, aim to address these challenges. Phase one focused on network industries, such as electricity and logistics, with notable improvements in energy supply with 150+ days of no loadshedding and green shoots in combatting the infrastructure challenges at Transet. The upcoming phase two will hopefully continue these reform agendas on the path to modernising services and enhancing efficiency and, ultimately, bolstering economic growth prospects.

Investment opportunities and risks

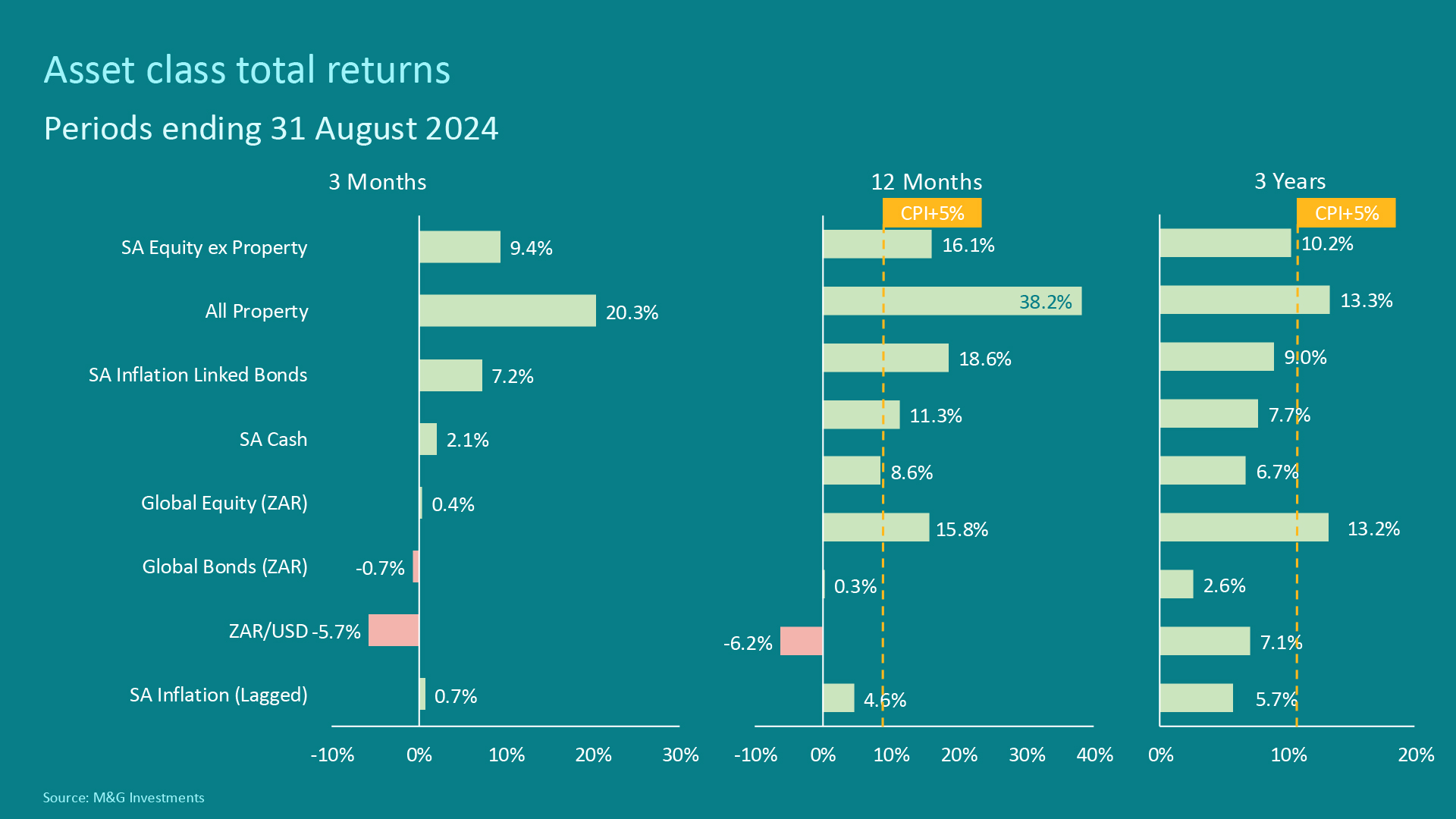

In global markets, global equities have delivered 15.8% (in rand), driven by a combination of decent earnings growth as well as a re-rating in broad equity markets. However, given the prevailing valuations across different equity markets, being selective in the markets you want to have active exposures in will be key – expensive equities rarely deliver continued outperformance. On the bond side, long dated US Treasuries look attractive, offering decent real yields to patient investors.

Looking to South Africa, equities have been viewed as value traps. However, when examining fundamental drivers such as dividend yields and real earnings growth, there is potential for solid returns. Despite recent price underperformance relative to global markets, South African equities offer favourable valuations compared to the increasingly expensive US market. The current sentiment-driven issues rather than fundamental weaknesses are impacting returns.

SA bonds have managed to deliver impressive returns at 18.6% over the last year and remain attractive. With yields offering nearly 6% real return, they present a compelling opportunity, even after the recent 200-basis-point (or 20%+ in total return terms) rally in bond yields in July and August. Given the prevailing cheapness, a further rally in yields would not surprise us at all.

The property sector has faced challenges, but recent market movements reflect a cautious optimism. Improved sentiment and expectations of easing interest rates have led to a rally in property stocks with 38.2% delivered for the latest one-year period, although this largely reflects market rerating rather than fundamental improvements.

Key takeaways:

- The global economic adjustment to higher interest rates is ongoing, with inflation proving more persistent than anticipated.

- South Africa’s structural reforms are making progress, with phase two crucial for sustained economic improvement.

- Improved sentiment towards South African assets post-election presents opportunities, though growth and policy reforms remain critical.

- While South African assets are undervalued, cautious optimism is warranted. Real yields on bonds are attractive and equities present potential for strong returns, but careful selection is necessary.

Conclusion

As we move through this period of heightened uncertainty and shifting economic regimes, it’s essential for South African investors to adjust their asset allocation strategies accordingly. The global inflationary environment and changes in monetary policy are reshaping market beliefs and thus asset pricing, requiring careful consideration of both local and international investment opportunities. Investors should remain vigilant, balancing optimism with caution as the economic landscape continues to evolve.

Share

Did you enjoy this article?

Get the Newsletter

Get the Newsletter