South Africa

South Africa Namibia

Namibia

Maryna Carstens

Equity Analyst

Something Brewing?

This article was first published in the Quarter 3 2022 edition of Consider this. Click here to download the complete edition.

Key take-aways

- Defying analyst predictions, spirits outperformed beer sales during Covid-19 and its aftermath as consumers opted to drink premium and super-premium brands at home despite lower incomes, continuing both the “premiumisation” and “slow volume growth” trends in the global market.

- Brewers have also faced a stronger US dollar, higher barley and energy costs, as well as supply chain disruptions. So rather than cost-cutting, they must focus on obtaining higher prices to improve their bottom lines. Also, developing countries where growth has greater potential have become more important than ever.

- We see Nigerian brewers as sound long-term investment cases given these companies’ greater growth potential and relatively cheap valuations currently. While we are very aware of country-specific risks, they benefit from the expertise of their global parents, among other upsides.

As has been true for most companies, the Covid and post-covid periods have been a challenging time for brewers. In South Africa, brewers were particularly hard-hit by the total ban on alcohol sales, a relatively rare phenomenon elsewhere in the world, and have subsequently seen large cost increases that have impacted their bottom lines. How have brewing companies fared amid these large demand and supply disturbances compared to their competitors and, as investors, where do we see value?

As has been true for most companies, the Covid and post-covid periods have been a challenging time for brewers. In South Africa, brewers were particularly hard-hit by the total ban on alcohol sales, a relatively rare phenomenon elsewhere in the world, while supply chain disruptions and lockdowns elsewhere led to large cost increases that have impacted brewers’ bottom lines. How have brewing companies fared amid these large disturbances compared to their competitors and, as investors, where do we see value?

Spirits versus beer

At the start of the Covid-19 pandemic, there was a large amount of uncertainty on how the global beer industry would be impacted. The general consensus was that spirits and beer would both experience reduced demand, resulting from travel restrictions and social distancing measures. However, as bars and restaurants were closed, the decrease in on-premise consumption was expected to be worse, together with downtrading into lower value categories due to lower consumer disposable income. As such, spirits, which is a category more exposed to the on-premise channel (i.e., it is consumed more in bars and restaurants and on social occasions), was expected to fare worse than beer.

Fast forward to 2022, and the words of Danish physicist Niels Bohr have once again proven true: “it is very difficult to predict — especially the future.”

While it is true that we saw a change in channel mix and a shift to “off-premise” or at-home consumption, several trends have emerged that were unforeseen and certainly not knowable.

One such trend was the exacerbation of premiumisation and the relative outperformance of the spirits market, as at-home consumption of premium and super premium spirits cushioned the fall in on-premise spirits sales. Surprisingly, consumers opted to spend their earnings on more up-market brands. In South Africa, post the lockdowns and alcohol bans, it became clear that demand was merely delayed and not destroyed. Brewer margins were also under pressure as the change in mix to off-premise consumption and cans rather than returnable glass bottles led to a global shortage of aluminium. Enter the tragic Russia-Ukraine war, and a new challenge emerged in the form of increased barley costs and an increase in energy prices. Add to this the backdrop of a strong US dollar and it is clear that brewers are facing one of the more challenging periods in their history. So where to from here?

Growth is harder to come by

Given our three- to five-year investment time horizon at M&G Investments, it is important to assess these trends and the current environment against the long-term history of the brewing industry to determine where we are in the cycle.

The global beer market is very consolidated, with the top five companies accounting for more than 56% of global market share. This compares to a highly fragmented spirits market, where the top five companies account for less than 31% of global market share, according to Morgan Stanley. Overall, the global beer market is mature, and looking at longer-term industry trends, volume growth has been hard to come by.

Given the size of the largest players and the concentration in the beer market, consolidation has also become harder to accomplish. Combine this with the global trend of premiumisation, and the global spirit players have emerged as clear winners in the post-Covid world with beer brewers’ market share theirs for the taking.

Looking at the problem beer brewers face simplistically, growth is a function of volume and price.

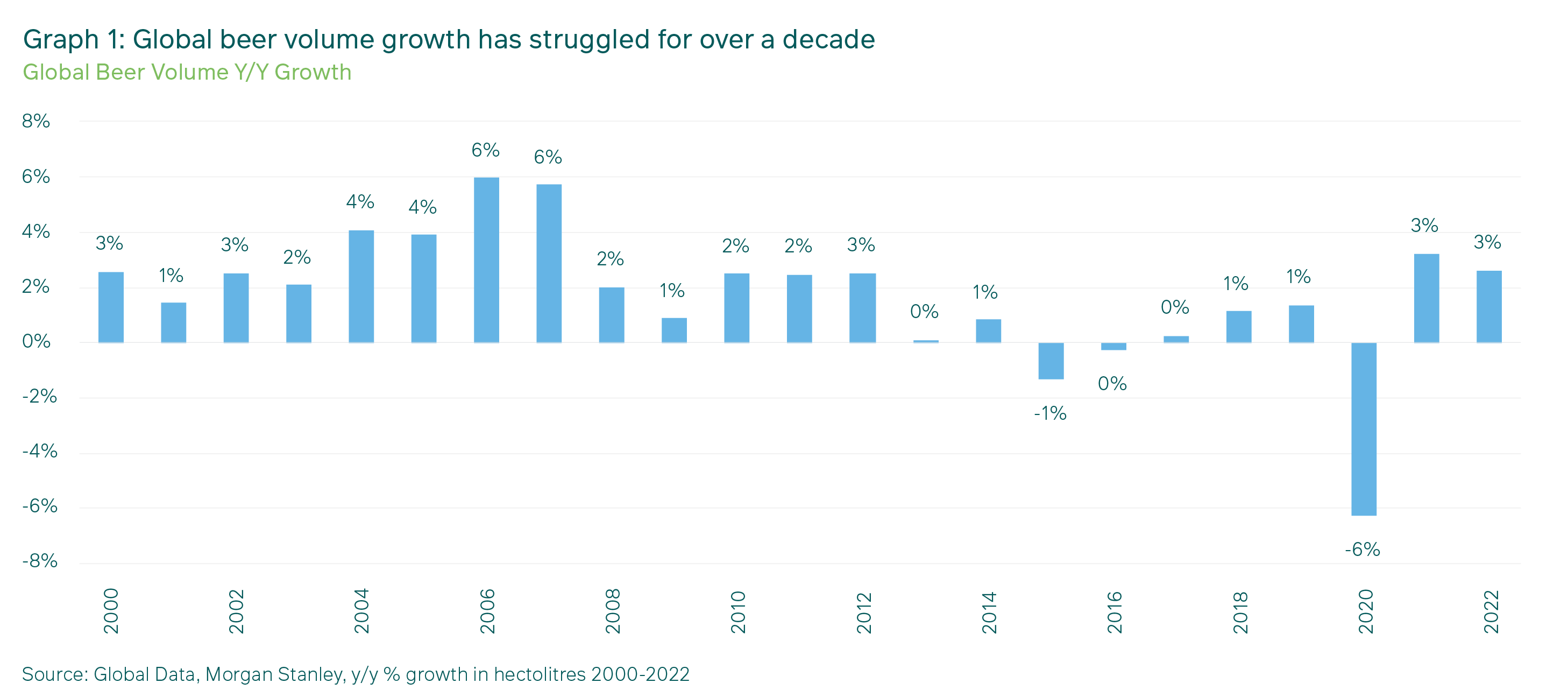

Click chart to enlarge

It is clear from Graph 1 that there has been very little volume growth in the global beer market over the last decade. This is a result of markets maturing and spirits and other beverages commanding a larger share of throat in mature markets.

Growth for the brewers must therefore come from price, either directly through price increases or indirectly through a change in sales mix by selling more of their pricier brands.

Premiumisation to the rescue?

This is where premiumisation comes into play. This trend is nothing new, but has become more important as beer companies have reached maturity in most of their markets. When a market premiumises, not only does share of throat shift from value or mainstream brands to premium or super-premium brands, but there is generally a shift from beer to spirits and other categories. Beer companies need to work harder and spend more just to maintain the same level of volumes. The brewer has to shift from being a traditional manufacturer and distributor, to becoming a consumer-focused brand protector and builder.

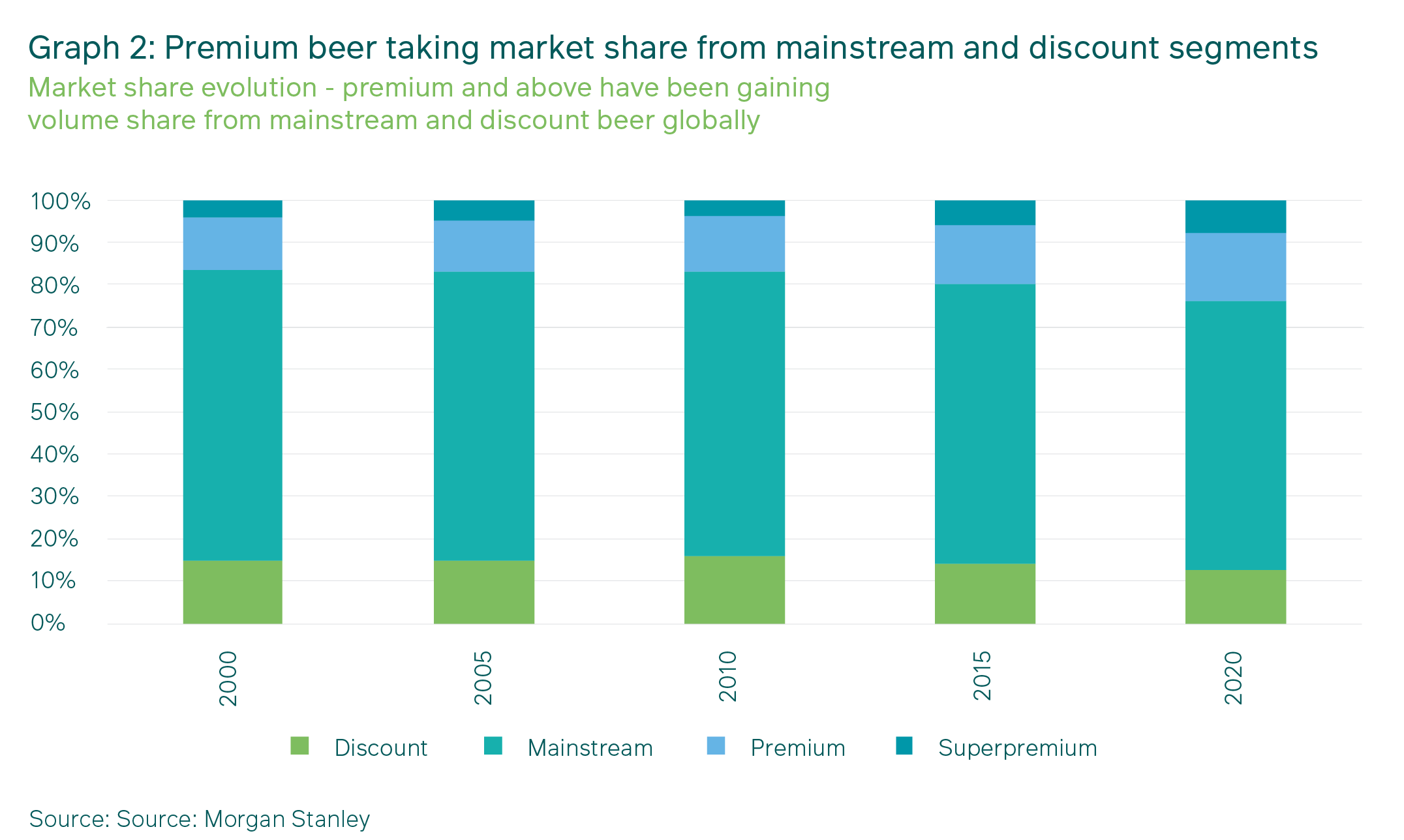

Click chart to enlarge

Graph 2 shows how more expensive beer brands have gradually been gaining ground from cheaper brands over the past 20 years. Premiumisation normally goes hand-in-hand with lower volumes and mainstream market share loss, but the company’s margin is protected to some extent as premium products demand a much higher selling price. Premium and super-premium products are more profitable than mainstream products, where differentiation is minimal, and consumers are more sensitive to price increases.

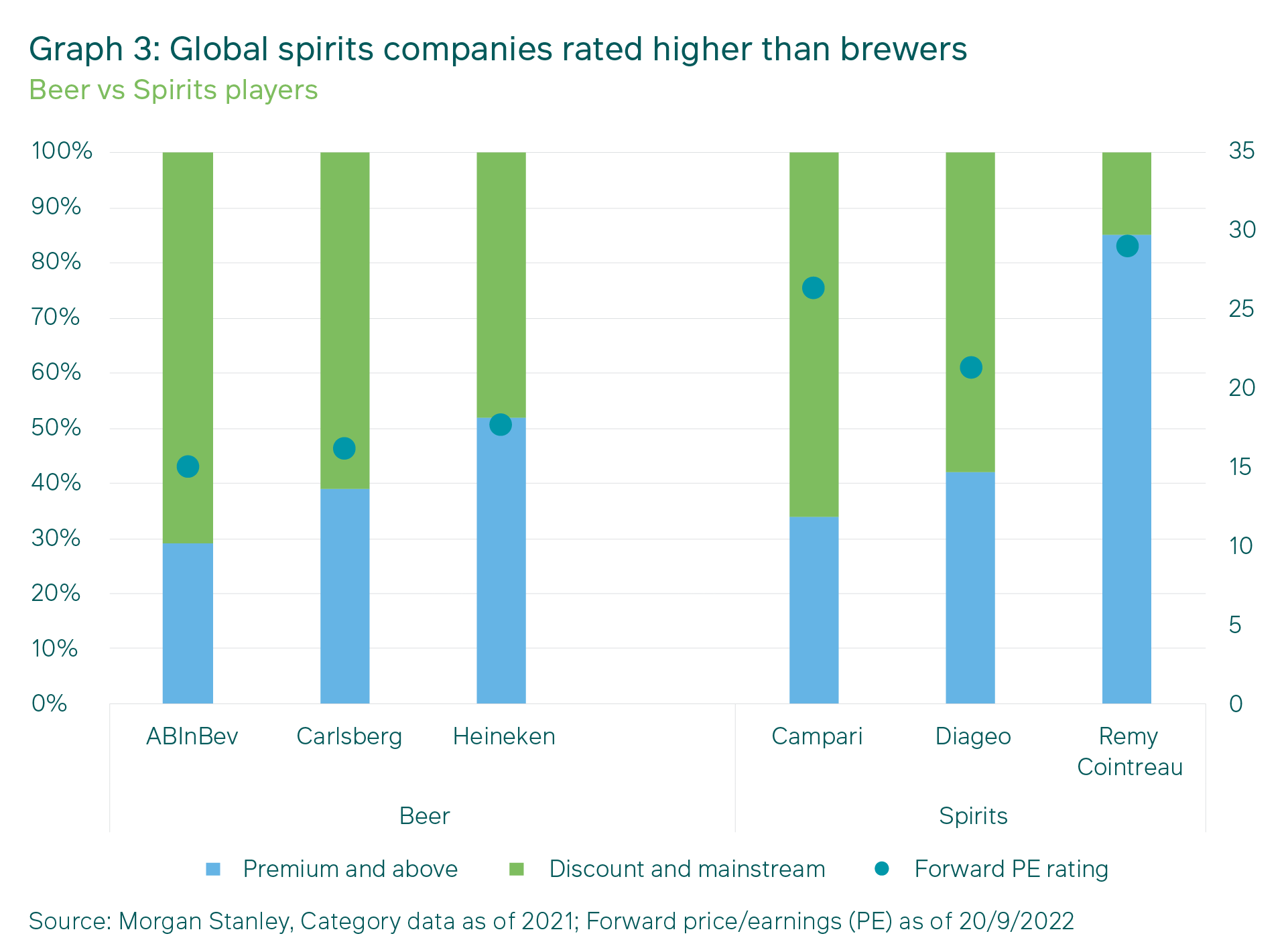

Not only do premium products come with a higher selling price, but the market is willing to attach a higher valuation multiple to companies that are more indexed to the premium and super-premium segments, as opposed to mainstream. In addition, spirits companies have in recent years commanded a valuation premium compared to their beer counterparts. Graph 3 highlights how the likes of Diageo, Remy Cointreau and Campari are trading at higher forward price/earnings (P/E) valuations than AB InBev, Carlsberg and Heineken. Also, Heineken’s higher mix of premium and super-premium products merits a higher market rating than its lower-market peers.

Click chart to enlarge

What about inflation?

Another element of price growth is inflation. Historically, brewers have generally been able to “price up with inflation” with relatively inelastic demand from consumers. Therefore, an inflationary environment is not necessarily negative for brewers, as higher selling prices are rather sticky and margin expansion can occur once cost headwinds eventually subside. In markets where this has not been the case and brewers have not been able to price with inflation, severe margin pressure has been evident.

What’s brewing in Africa?

Bringing the argument closer to home, in a global landscape where volumes are not growing, Africa has emerged as an important growth market, as its demographics are key to unlocking future volume growth for the industry. It is therefore no surprise that the global beer players ABI, Heineken and Castel, and the spirits player Diageo are well represented in Africa.

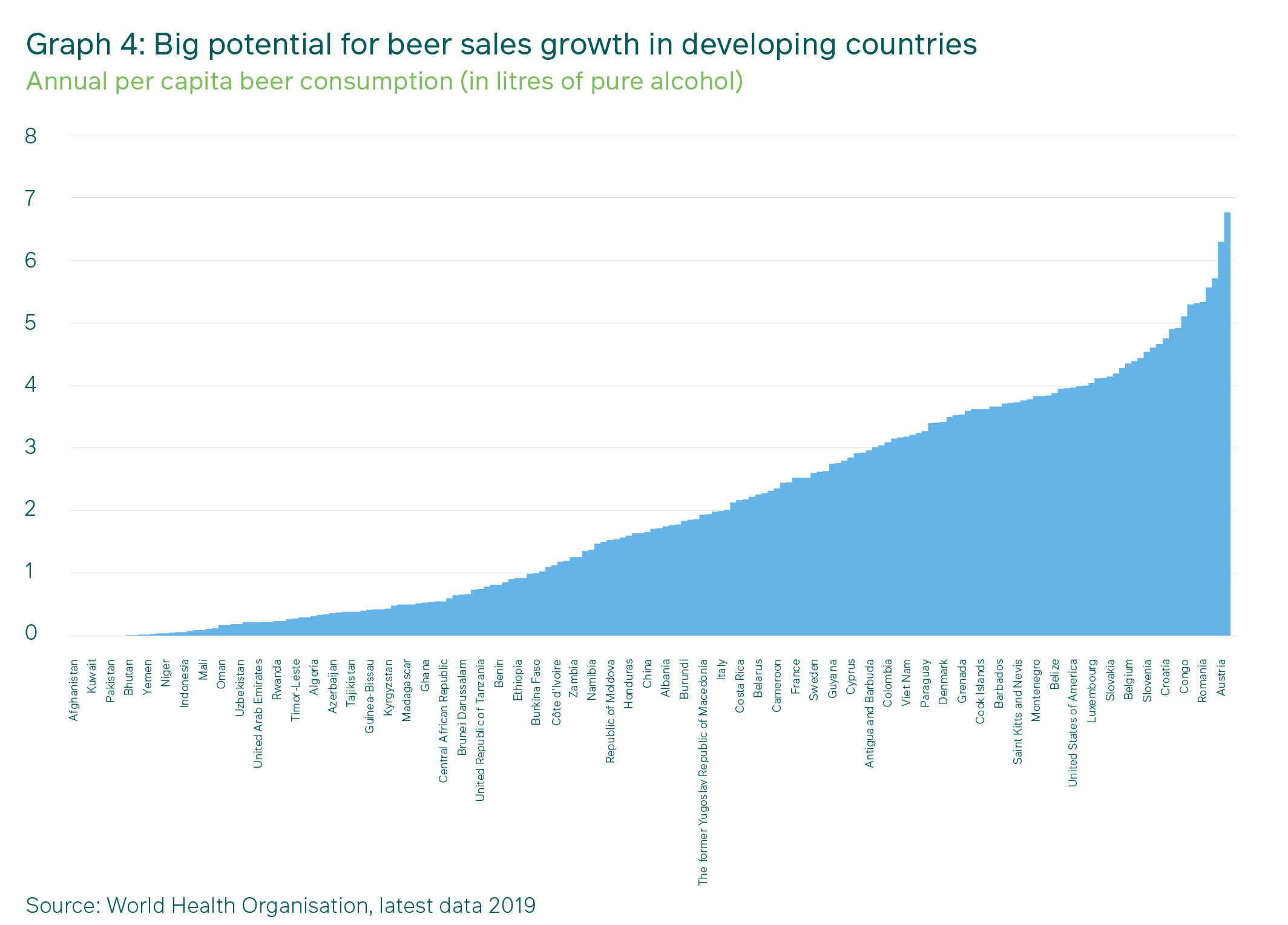

The largest market on the African continent is Nigeria. It is still in its early maturity market phase, with low per capita consumption and favourable demographics. From Graph 4 it is clear that there is still significant room for per capita beer consumption growth, with Nigerian drinkers consuming less than one litre of beer annually compared to their Polish counterparts at nearly seven litres (as measured in litres of pure alcohol).

Click chart to enlarge

Understanding the Nigerian beer market

The formal brewer market in Nigeria is dominated by three large players: Nigerian Breweries, the largest player in the market with more than 55% market share, a subsidiary of Heineken; Guinness Nigeria, a subsidiary of global spirits player Diageo; and International Breweries, a subsidiary of AB InBev.

The Nigerian market has been a case study in value destruction. At the height of the market cycle in 2013, the combined market capitalisation of the three large brewers was almost US$ 12 billion. Today, these brewers are valued at less than US$2 billion.

This has in large part been due to the continuous depreciation of the Naira and a lack of US dollar earnings growth, with around 50% of brewing raw material costs directly or indirectly linked to the US dollar. In order to protect margins in a market experiencing currency weakness, a lack of dollar availability and high local inflation, it is imperative to be able to put through price increases.

Up until recently In the Nigerian market, this has not been possible. Instead, a weak consumer environment and capacity additions led to a price war that destroyed the profitability of these brewers. This was clearly not sustainable. At the low levels of profitability at which these brewers operated, it was hard to justify continuing operations at all, as the cost of capital in Nigeria by far exceeded the returns earned. This scenario is now reflected in the companies’ very low share prices.

Taking advantage of value

In the M&G Africa Equity Fund, we own a handful of African brewing companies, with our largest overweights being in Nigerian Breweries and Guinness Nigeria. Where appropriate, other M&G unit trusts also have exposure to these stocks via underlying holdings in the M&G Africa Equity Fund.

At the height of the pandemic, Nigeria Breweries traded below US$50 on an enterprise value per hectolitre basis. This is far below our deemed replacement value of US$200 per hectolitre of brewing capacity, and does not reflect the value of its distribution network, in-country malting plants, brand strength or latent growth in the market.

Our interest was piqued when it became clear that rationality was returning to the market and that the brewers were able to increase selling prices across the board. This, together with volume growth, led to improved profitability levels that are not reflected in the share prices.

We increased our position in Guinness Nigeria when it became clear they were executing on their strategy to focus on their core capabilities of spirits and stout, and exiting the overcrowded lager market. International Breweries and Nigerian Breweries were also able to push through price increases, and because of the significant operational leverage in these companies, the impact on returns was immediate.

Without getting into the details of the Nigerian macro environment, which is a topic for another day, it is important to note that we do not wear rose-coloured glasses when it comes to Nigeria. We continue to foresee challenges in this market as the structural issues in the economy remain, and the country has not fully benefitted from the higher oil price environment due to low production levels caused by a lack of investment.

However, even after taking all these risks into account, we, like the global brewing companies who have recently added incremental in-country capacity, recognise the attractiveness of the market and potential for long-term growth. Recent deals such as the Heineken-Distell transaction or Diageo’s announced sale of its Cameroon subsidiary to Castel were done at valuation levels much higher than where the Nigerian brewers currently trade, highlighting the attractiveness of these assets.

Like brewing itself, the value to be unlocked from these shares might be a long and exacting process, but at today’s very attractive valuation levels, we believe the odds are skewed in our favour to achieve outsized returns in the medium to long term.

Share

Did you enjoy this article?

Get the Newsletter

Get the Newsletter